NewsBaza

IT and Technology News

Toggle navigation

News

Finances

Medicine

Men’s Guide

Geek Guide

Livejournal

Marketing

Design

infboom.ru

oxak.ru

obsigen.ru

×

Browsing posts tagged: Finances

Backdoor Roth IRAs Really a Smart Idea?

evergreensmallbusiness.com

Finances

Estimating Investment Portfolio Returns and Values

evergreensmallbusiness.com

Finances

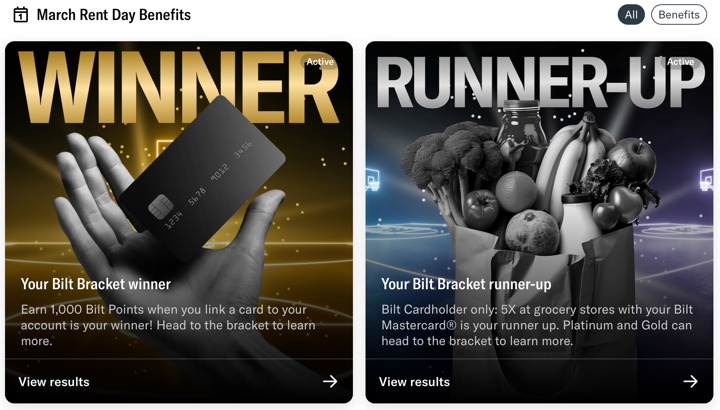

Bilt Mastercard: Earn Rewards For Paying Rent w/ Any Landlord (March 1st Promo, Easy 2,000 Points)

mymoneyblog.com

Finances

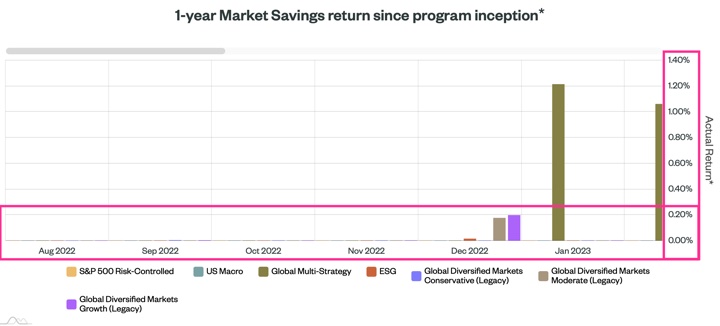

Save App Review: 9.07% APY Advertised vs. 0.00% APY Experienced (Historical Results Now Posted)

mymoneyblog.com

Finances

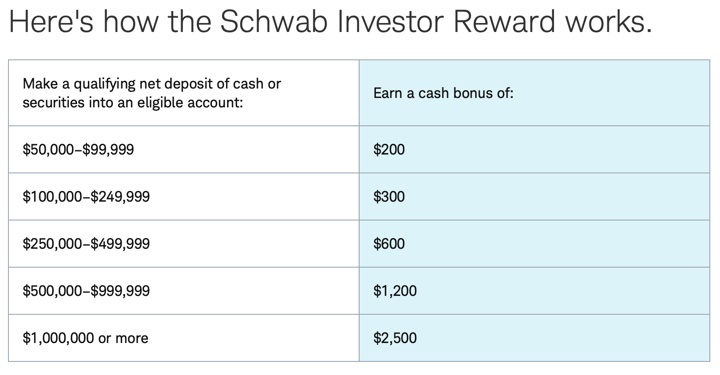

Charles Schwab Brokerage: Up to $2,500 New Deposit / Transfer Bonus (New & Existing Customers)

mymoneyblog.com

Finances

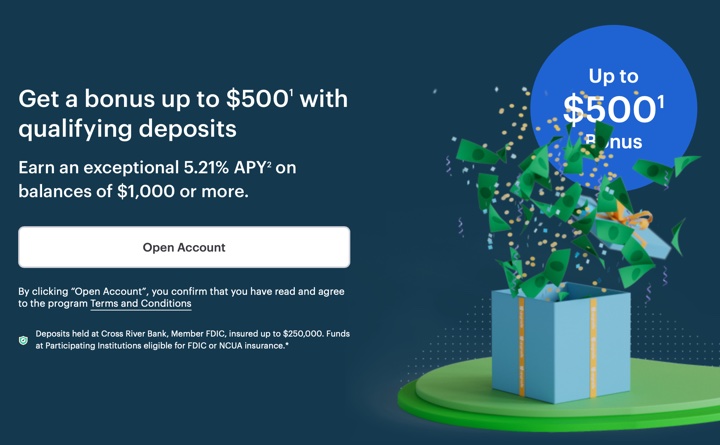

Upgrade Premier Savings: Up to $500 Deposit Bonus + 5.21% APY (Improved)

mymoneyblog.com

Finances

IKEA Family Discount: $15 off $150, $30 off $300, $50 off $500 (Ends 3/3/24)

mymoneyblog.com

Finances

Wells Fargo $325 Checking + $225 Savings Account Bonuses

mymoneyblog.com

Finances

Cummins & Atmus Filtration Odd Lot Tender Opportunity / Exchange Offer

mymoneyblog.com

Finances

Study: 100% Stocks The Best Portfolio For Both Accumulation and Retirement Income?

mymoneyblog.com

Finances

Amtrak Guest Rewards Preferred Mastercard: 40,000 Point Offer (Worth $1,000 in Amtrak Fare or $400 in Amazon Gift Cards)

mymoneyblog.com

Finances

CFP Course Notes: The 7-Step Financial Planning Process

mymoneyblog.com

Finances

Top 10 Best Small Business Credit Card Bonus Offers – February 2024

mymoneyblog.com

Finances

Marriott Bonvoy Business® American Express® Card Review: 5 Free Night Awards Offer (Worth Up To 250K Total Points)

mymoneyblog.com

Finances

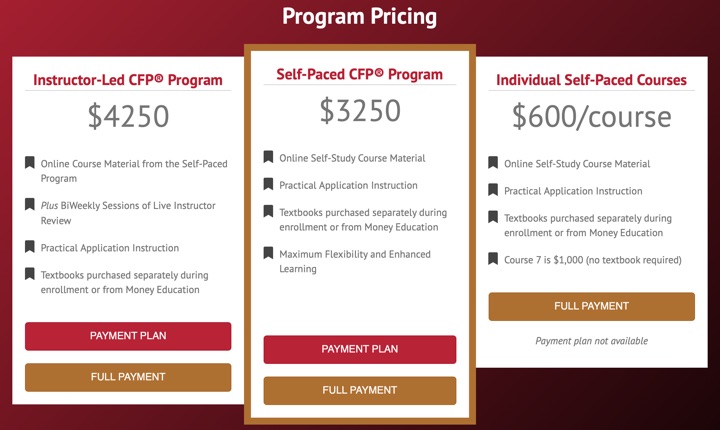

Taking a Self-Paced CFP Education Course For Fun and… Personal Knowledge

mymoneyblog.com

Finances

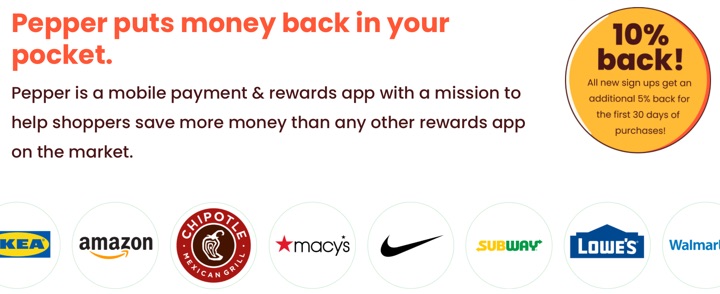

Pepper Rewards App: $20 Referral Promo Code + 10% Back = $130 of Amazon Gift Cards for $100

mymoneyblog.com

Finances

TurboTax Online Walkthrough: How To Enter US Treasury Interest from Money Market and Bond Funds/ETFs For State Tax Exemption

mymoneyblog.com

Finances

IHG One Rewards Premier Card Review: 165,000 Bonus Points Limited-Time Offer

mymoneyblog.com

Finances

IHG One Rewards Traveler Card Review: 100,000 Bonus Points Offer, No Annual Fee

mymoneyblog.com

Finances

Best Interest Rates on Cash – February 2024

mymoneyblog.com

Finances

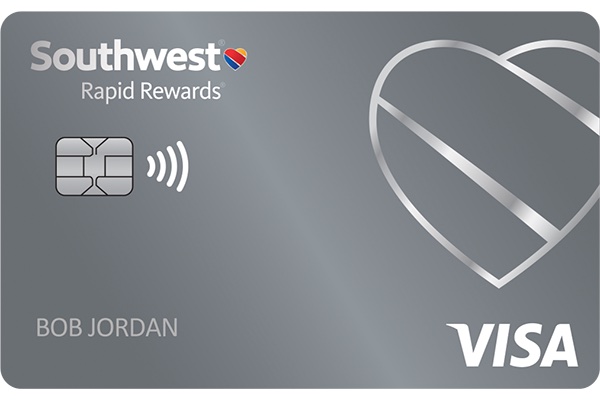

Southwest Airlines Credit Cards: Limited-Time Offer for Companion Pass Thru 2/28/25 + 30,000 Points

mymoneyblog.com

Finances

Laurel Road High Yield Savings Deposit Bonus: 5.00% APY + Up to $200 (Referral Only)

mymoneyblog.com

Finances

Amazon Audible: Free 3-Month Trial w/ 3 Free AudioBooks (New & Returning)

mymoneyblog.com

Finances

How To Afford a House These Days

mrmoneymustache.com

Finances

Top 10 Best Credit Card Bonus Offers – February 2024 (Updated)

mymoneyblog.com

Finances

Monte Carlo Safe Withdrawal Rates for Low Expected Returns

evergreensmallbusiness.com

Finances

More Data in Support of Buy and Hold Investing

mymoneyblog.com

Finances

Vanguard Federal Money Market Fund: How to Claim Your State Income Tax Exemption

mymoneyblog.com

Finances

Bilt Mastercard: Earn Rewards For Paying Rent w/ Any Landlord (February 1st Promo, Aeroplan Transfer Bonus)

mymoneyblog.com

Finances

“Tune Out the Noise”: A Film about Index Funds and Dimensional Fund Advisors (DFA)

mymoneyblog.com

Finances

Callan Periodic Table of Investment Returns 2023 Year-End Update

mymoneyblog.com

Finances

United(SM) Business Card Review: New 100,000 Bonus Miles Offer

mymoneyblog.com

Finances

Robinhood IRA Transfer and 401k Rollover 3% Bonus Match (No Cap)

mymoneyblog.com

Finances

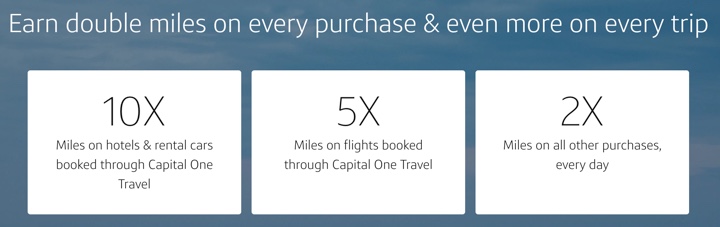

Capital One Venture X Business Card Review: New 300,000 Miles Intro Bonus (Worth $3,000 Towards Travel)

mymoneyblog.com

Finances

Best 0% APR Balance Transfer Credit Cards – Updated 2024

mymoneyblog.com

Finances

Consistently Investing $850 a Month x 10 Years = $160,000 (2014-2023)

mymoneyblog.com

Finances

Top 10 Best Credit Card Bonus Offers – January 2024 (Updated)

mymoneyblog.com

Finances

Top 10 Best Small Business Credit Card Bonus Offers – January 2024

mymoneyblog.com

Finances

Alaska Airlines Visa Credit Card: 70,000 Miles + $122 Companion Fare

mymoneyblog.com

Finances

Ally Bank Deposit Bonus: 0.50% of New Deposits, Up to $125 (New Customers via Referral Only)

mymoneyblog.com

Finances

Navy Federal Flagship Travel Rewards Credit Card: 35,000 Bonus Points, Year of Amazon Prime, 2X Points

mymoneyblog.com

Finances

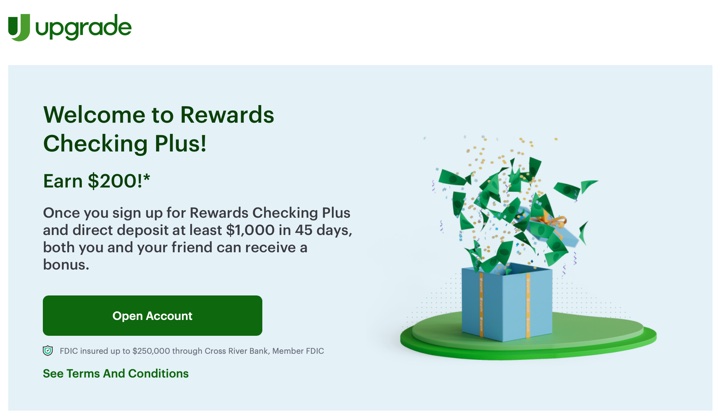

Upgrade Rewards Checking $200 Referral Bonus + 5.07% APY Savings

mymoneyblog.com

Finances

Save App Review: 9.07% APY Advertised vs. 0.00% APY Actual?! My Experience

mymoneyblog.com

Finances

$6,500 IRA Contribution Bonus Challenge: $5,444 in Bonuses (2023 Year End)

mymoneyblog.com

Finances

M1 Finance Review: Free Robo-Advisor, M1 Plus Price Drop, New $250 and 401k/403b/457 Rollover Bonuses

mymoneyblog.com

Finances

Best Interest Rates on Cash – January 2024

mymoneyblog.com

Finances

Chase Ink Business Cash(R) Card Review: $900 Bonus (Highest Ever), 5% Back Categories, No Annual Fee

mymoneyblog.com

Finances

MMB Portfolio Dividend & Interest Income Update – Year-End 2023

mymoneyblog.com

Finances

iPhone 6/7/SE Performance Slowdown Class Action Settlement

mymoneyblog.com

Finances

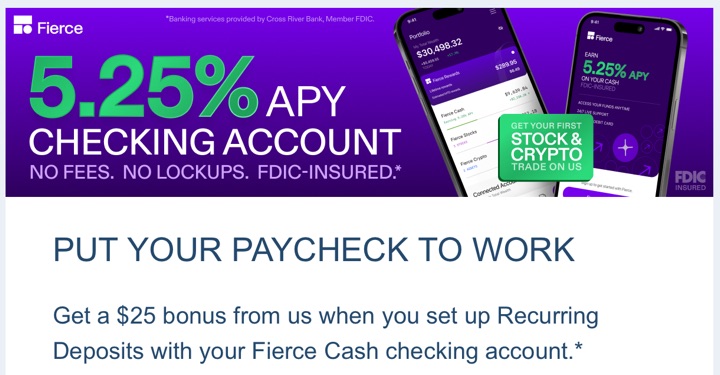

Fierce Finance App Review: 5.25% APY + New Deposit/Referral/Trade Bonuses

mymoneyblog.com

Finances

Fidelity Bloom App: Fintech App from Traditional Broker ($30 Savings Match for 2024)

mymoneyblog.com

Finances

2024 Retirement and Benefit Plan Limit Increases: 401k, 403b, IRA, HSA, DCFSA

mymoneyblog.com

Finances

2023 Year-End Review: Annual Broad Asset Class & Target Fund Returns

mymoneyblog.com

Finances

Bilt Mastercard: Earn Rewards For Paying Rent w/ Any Landlord (January 1st Promo, Airline Transfer + Amazon)

mymoneyblog.com

Finances

HealthyWage Review: Bet on Yourself, Get Paid To Lose Weight ($50 Limited-Time Prize Boost)

mymoneyblog.com

Finances

BOI reports and Your Small Business

evergreensmallbusiness.com

Finances

TurboTax Desktop 2023: Deluxe Federal & State $45 w/ $10 Amazon Gift Card (Premier $65 w/ $10 GC)

mymoneyblog.com

Finances

Worried about Overfunded 529 Balances? The Half-Time Community College Method

mymoneyblog.com

Finances

Top 10 Best Small Business Credit Card Bonus Offers – December 2023

mymoneyblog.com

Finances

Top 10 Best Credit Card Bonus Offers – December 2023 (Updated)

mymoneyblog.com

Finances

« Previous