Eventually, you will be presented with the idea of writing covered calls on your portfolio and earning “easy income” from this strategy. I already know intuitively that there must be a cost to this “passive income” and that the net effect is worse performance than simply holding the same index fund or stock for the long term. However, the pushback is usually that you can get a more reliable cashflow in exchange for giving up some of your upside.

The article (via ) does a good job of explaining why there is unfortunately no “free lunch” with this strategy, even if your goal is to create steady income.

Many investors focus on the call premium as a source of portfolio “income” while still participating in a limited amount of appreciation of the stock. As long as the stock stays below the strike price and the call expires worthless, the strategy can generate positive portfolio income, making it ideal for flat or down markets. However, trying to time when stocks and markets will be flat or down is extremely difficult, particularly given the long-term upward bias of the equity markets. As such, there is a hidden cost of covered call writing, which is the potentially significant opportunity cost of having the stock go above the strike price causing lost portfolio appreciation.

Covered calls work great when they work out, since you get to keep your stock and the “free income”. Giving up your upside may seem like a good deal, but you must realize that much of the stock market’s return comes from lumpy periods where it shoots up without warning.

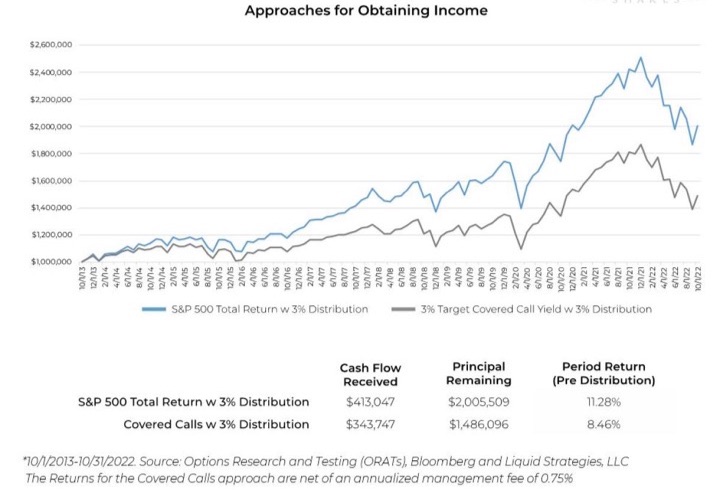

The chart below from the article compares the performance results between simply withdrawing 3% a year from your S&P 500 portfolio from 2013 to 2022, as opposed to writing covered calls with a 3% yield on your S&P 500 portfolio. The chart does add a 0.75% annual management fee for this approach, but even if you add that back in, the difference is still 11.3% vs. 9.2% annualized return.

Lower volatility is also commonly cited as a benefit of a covered call strategy. Well, yeah, if you limit your upside every time the strike price is exceeded, then you will have lower volatility.

In a rising market, covered calls may actually reduce upside portfolio volatility, which is the type of volatility that investors benefit from. As such, when evaluating covered call strategies that show lower volatility statistics than the broader market, investors should be mindful of where that volatility reduction may be coming from.

Am I willing to give up 2% in annual returns for a steady income? Nope. I mean, 2% is already roughly the entire dividend yield of the S&P 500. The problem is that most people who use this strategy aren’t properly tracking their performance and probably don’t want to know that they are lagging behind simple buy and hold. The call premium income comes in most of the time, except for when it doesn’t.

There are certainly scenarios where if you think you have an information edge, knowing how to structure an option can help you make the right bet. But they aren’t magic! I am very skeptical of the idea of any options strategy that will somehow give you reliable income without a significant cost of hurting your total returns. That just gives me the same feeling of someone who claims to invent a machine that defies a basic law of physics.

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2004-2022 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.