Per , a financial “hedge” is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. Wouldn’t be nice if for every Investment A, there was another Investment B that would always move in the opposite direction? Unfortunately, things aren’t so easy.

Per , a financial “hedge” is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. Wouldn’t be nice if for every Investment A, there was another Investment B that would always move in the opposite direction? Unfortunately, things aren’t so easy.

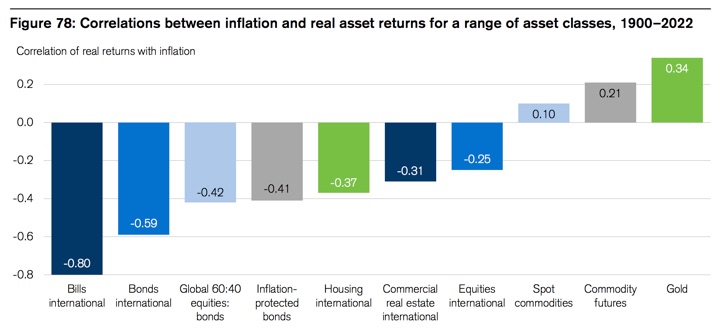

A common question: Should we own stocks as a hedge against inflation? The Institutional Investor article provides a little of clarification:

“Equities are not an inflation hedge. When inflation is high, they tend to do poorly. But in the long run, they have beaten inflation, so a lot of people claim they’re an inflation hedge, but [that claim is the result of confusion]. In the long run, stocks beat inflation, but they do it because of the equity risk premium. They are not an inflation hedge. They have a negative correlation with inflation,” said Marsh.

Historically, stocks actually tend to go down when inflation goes up.

Here’s a chart of the correlations between inflation and various asset classes over the last 120+ years from the :

Here is Warren Buffett in his 2022 Berkshire Shareholder letter (emphasis mine):

During the decade ending in 2021, the United States Treasury received about $32.3 trillion in taxes while it spent $43.9 trillion.

Though economists, politicians and many of the public have opinions about the consequences of that huge imbalance, Charlie and I plead ignorance and firmly believe that near-term economic and market forecasts are worse than useless. Our job is to manage Berkshire’s operations and finances in a manner that will achieve an acceptable result over time and that will preserve the company’s unmatched staying power when financial panics or severe worldwide recessions occur. Berkshire also offers some modest protection from runaway inflation, but this attribute is far from perfect. Huge and entrenched fiscal deficits have consequences.

We can’t predict inflation, and we can’t expect stocks to go up when inflation does hit. However, we depend on businesses as a whole to continuously adapt (raising prices, lowering input costs, switching to alternative products, etc), so our best choice is to hold stocks and hope they continue to adapt through capitalism. If we only hold cash, we can only expect to break even after inflation at best, and usually go negative after taxes.

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

from .

Copyright © 2004-2022 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.