I can’t recall the exact source or quote, but I read something along the lines of this in a forum recently:

I can’t recall the exact source or quote, but I read something along the lines of this in a forum recently:

We don’t really want to hear other people’s opinions. We want to hear our own opinions out of other people’s mouths.

In other words, confirmation bias:

(source: )

The majority of my portfolio is in low-cost, diversified, passive-managed mutual funds. In order to hear a different take, I read the (Southeastern Asset Management), which are respectable examples of higher-cost, concentrated, actively-managed mutual funds. The managers “eat their own cooking”, meaning they put a substantial portion of their personal net worth into the funds. They have a limited number of holdings, try to avoid asset bloat, and try to outline their positions in shareholder letters.

In their most recent [pdf], they share a presentation that explains their position:

Why We Believe Active Long-Term Value Investing in Common Stocks Will Actually Work

Active investing is out of favor; long-term investing (or really, long-term anything) is out of favor; value investing as we practice it is out of favor; and, investing in common stocks is out of favor compared to private equity. Doing all four of these things really makes us the skunk at the party.

Many have given up on active, long-term, engaged value investing in public equities just at the point when we believe it offers the best risk/reward proposition. Indexing’s multi-year momentum has pushed more assets into fewer stocks because they have gone up and left behind an expanding universe of highly competitive, well-governed and managed businesses with unique advantages that are materially underpriced in their publicly traded securities.

They make several interesting points, including the high amount of “closet indexers” out there. (Haven’t there always been a lot of closet indexers though?) I tried to see things from their perspective, but in the end I think their 1% expense ratio is just too high to overcome. It will definitely take a bear market for their performance gap to narrow.

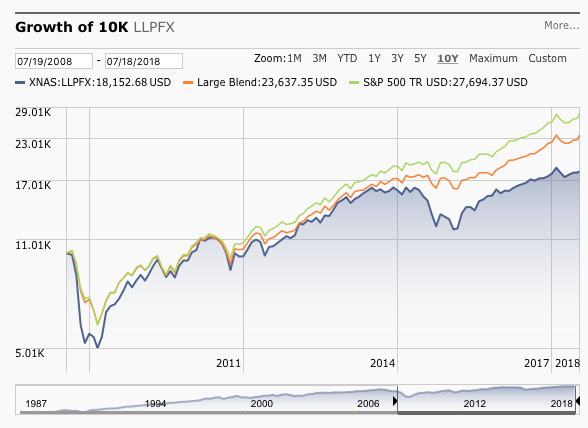

In the meantime, their real problem is that poor relative performance. For every $10,000 invested in their flagship Partners fund 10 years ago, you would have about $18,000 today. If you had put it in a low-cost S&P 500 index fund, you would have about $27,000 today. That’s the difference between 6% and 10% annualized returns over the last 10 years. The extra drag from their ~1% expense ratio accounts for about a quarter of the performance gap.

Longleaf Partners Fund very well might turn things back around. I have no position in any of their funds, but I’ll keep reading their free shareholder letters and watch them try their best to play a very difficult game.

from .

© MyMoneyBlog.com, 2018.